Yen Speculation

Yen Speculation

The BoJ's trilemma, the Fed, and the yen

In the movie Castaway, the main character (played by Tom Hanks) is stranded for years on a remote island in the Pacific.

Eventually, he resolves to leave the island and builds himself a raft. However, his attempts to take to the open ocean are frustrated by strong incoming waves at the point where the ocean meets the coral reef his island is enclosed by. His raft capsizes, and he’s beaten back.

That’s the image that came into my mind in early August, when Bank of Japan deputy governor Uchida issued a kind of Bank of Japan put following the major, if short-lived, global market ructions of the days before.

In particular, he strongly conditioned the future path of monetary policy in Japan on the outlook for the economy and prices which, in turn, he described as a function of stock prices and exchange rates.

While this isn’t very different from what any central bank says, the context matters.

Here’s a central bank trying to change course after many years – nay, decades – of ultra-loose monetary policy; and it faces violent market moves, particularly in what’s probably the single most important price for the Japanese economy: the yen exchange rate.

In short, a central bank trying to change course is faced with adverse market developments that at least call into question its ability to maintain the new course.

Dominated?

To this former central bank economist, the episode sounds an awful lot like a case of financial dominance.

Loosely speaking, financial dominance is a situation where financial fragility – the prospect of large losses in the financial sector and/or significant market volatility – prevents a central bank from tightening policy.

Of course, with markets more quiescent, BoJ officials have again begun signaling further tightening — but the conditionality, and hence the put, is always there. And the yen is rallying in response to such pronouncements.

To me, this looks a bit like a cat and mouse game (you decide who’s the cat and who’s the mouse).

What’s more, financial dominance can be connected to fiscal dominance – fiscal authorities’ lack of ability (or willingness) to exercise fiscal restraint limiting the central bank's ability to tighten policy.

So what I want to do in this post is to try to unravel the Japan macro conundrum from the angle of the constraints to its policy that the BoJ may be subject to.

To do that, I will start with a (selective) recap of the whys and wherefores of Japan’s policy mix.

Japan policy mix speed read

The BoJ has been keeping JGB yields low through zero or negative policy interest rates and quantitative easing for many years, culminating in yield curve control (YCC).1

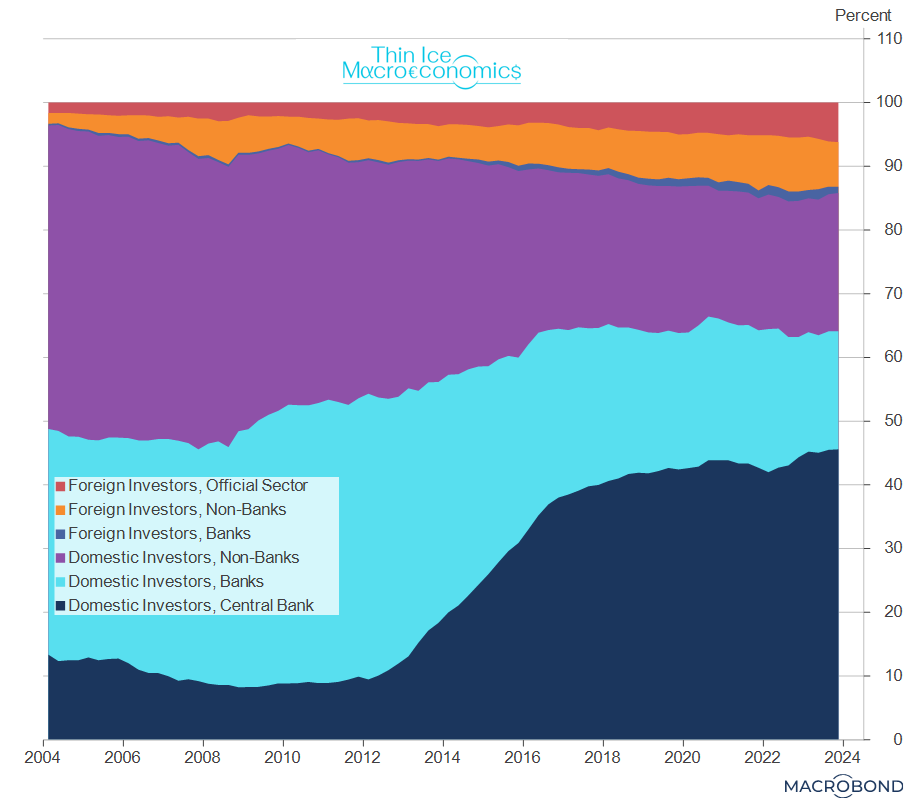

These policies have resulted in a rotation of Japanese government debt ownership from mostly the Japanese private sector – domestic banks, domestic non-banks – to the BoJ.2

source: IMF, Macrobond

The – not entirely unintended – byproduct has been to finance the government cheaply (as everywhere else). Saving on interest expenses means the government wouldn’t have to touch politically difficult parts of spending such as social security in an aging society.

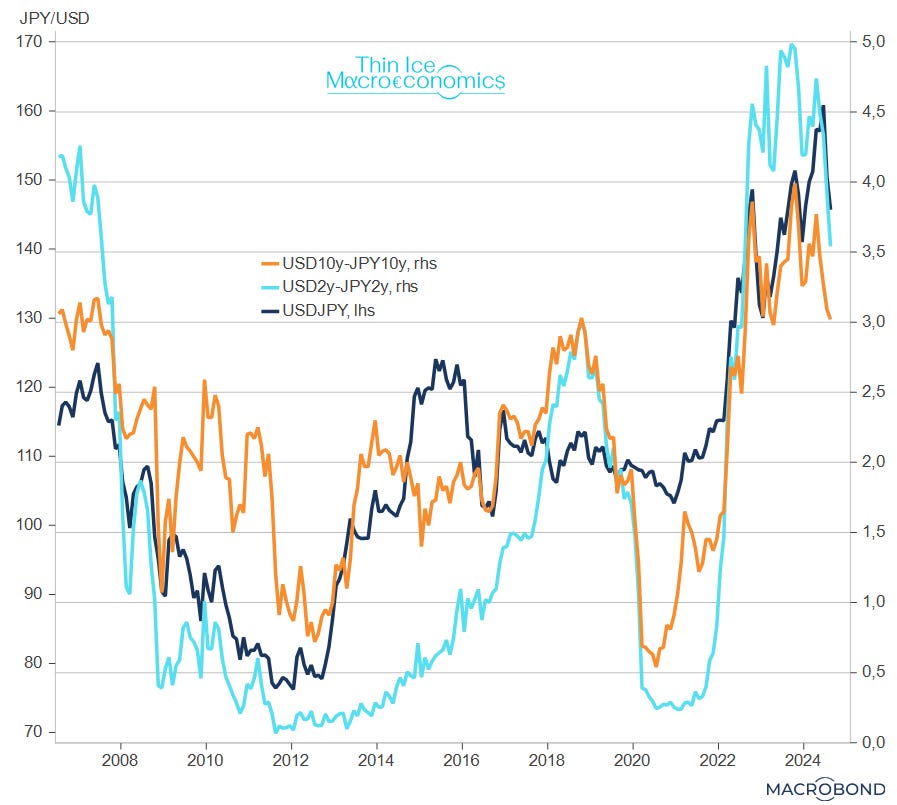

However, suppressing domestic interest rates has resulted in large interest rate differentials vis-à-vis other economies, leading to a weak yen – the inevitable result of pegging the interest rate while maintaining full capital mobility.

This weakness of course became particularly acute recently as other central banks raised rates to fight inflation, while the BoJ stayed pat.

source: Federal Reserve, Macrobond

The other side of this coin is that domestic players kept investing their money abroad, where they got better returns.

In short: Japan’s been trying to have its cake and eat it (don’t we all?) by financing its government cheaply, while asset holders enjoy the benefits of an open capital account, i.e. higher returns abroad.

The stock gain and the flow pain

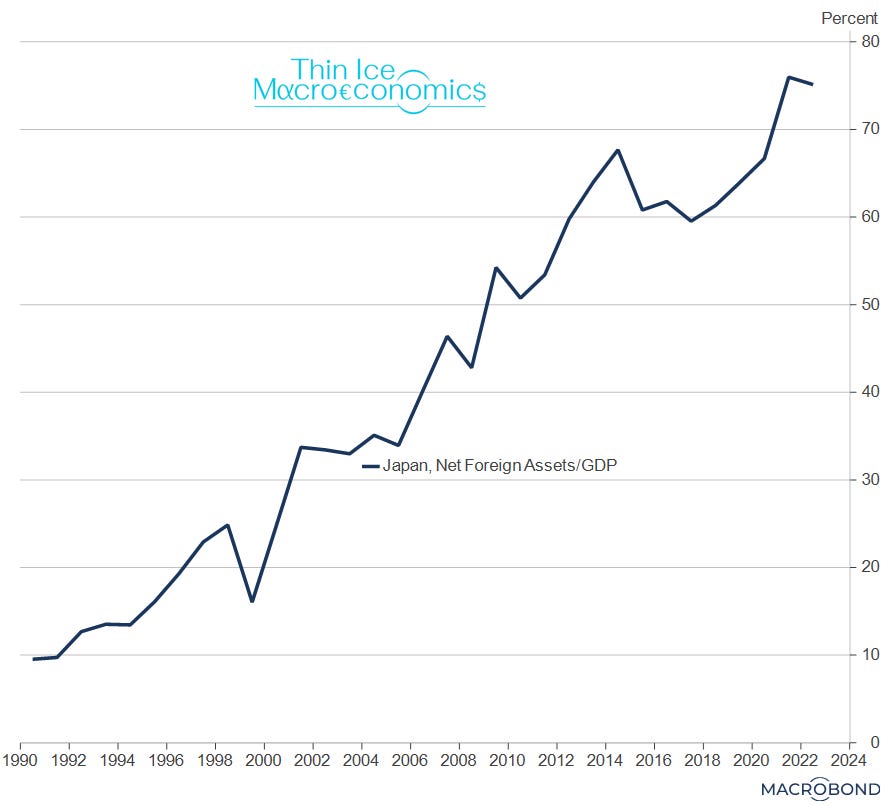

Now, Japan is the world’s largest net creditor – net foreign assets are about 500 trillion yen or 75% of the country’s GDP (or about 3% of global GDP).

The Japanese economy – including the government with its 1 trillion dollars of foreign exchange reserves – is massively long foreign currency.

source: Hutchins Center (External Wealth of Nations), Macrobond

So yen depreciation actually means large – albeit in aggregate unrealized – valuation gains for the foreign asset holders: domestic savers, corporates who have done FDI abroad, and the government. That’s a stock effect.

However, a weakening currency also means a negative income shock (a flow effect). Imports – not least of energy – become more expensive. Importantly, unlike the (mostly) valuation paper gains on foreign assets, this pain is realized – it lowers real income. And it does so for all domestic citizens.

So one way to look at the policy regime change we are witnessing is that it is the result of the pain of the YCC/weak–yen policy mix exceeding the gain.

And the nexus between fiscal sustainability and financial stability in an economy with an open capital account (free flow of capital) becomes apparent. The BoJ’s efforts to suppress JGB interest rates in order to maintain fiscal sustainability provide impetus for the yen carry, which in turn challenges financial stability.

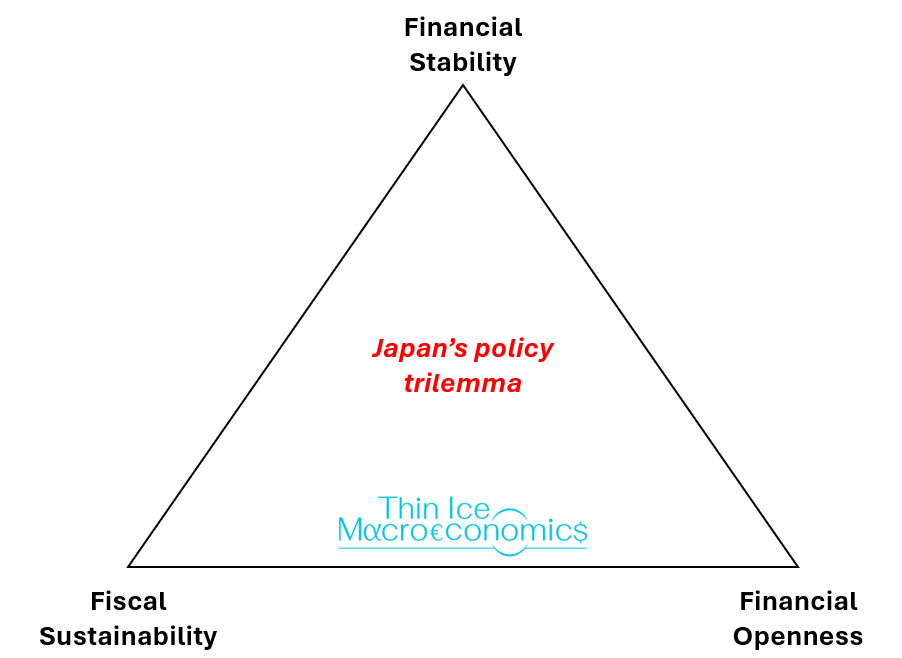

The BoJ’s trilemma

A trilemma is a situation where you can only ever have two of three desired items. (A trilemma is not a situation where you don’t know what to choose out of three available options – cake, ice cream, or chocolate. It’s a situation where you can have any two, but not the respective third.)

Let’s see how this works in the case of the BoJ.

The policy objectives — depicted in a triangle below — are Financial Stability, Financial Openness (or free capital flows), and Fiscal Sustainability.

source: Thin Ice Macroeconomics

The three facets of the trilemma are as follows.

Japan can have fiscal sustainability (lower yields on JGBs through the Bank of Japan’s YCC) and financial openness (allowing Japanese asset holders to take advantage of higher returns abroad) – but this gives impetus to the yen carry, eventually endangering (global) financial stability.

If the BoJ doesn’t engage in YCC, and Japan remains financially open, the yen carry is thwarted or at least attenuated. But interest rates on Japanese government debt will be closer to global rates, potentially calling into question fiscal sustainability.

Finally, if Japan wants to maintain a low interest rate on its government debt to ensure fiscal sustainability, as well as maintain financial stability, it can restrict its financial openness. That would decouple domestic from global rates and limit the yen carry, but at the expense of Japan’s asset holders, who can no longer enjoy higher returns overseas.

Readers who, like me, are into trilemmas (everyone’s entitled to a vice in life!) will recognize this as a variant of the financial trilemma involving

National control over financial policies (in Japan’s case: the BoJ suppressing interest rates on JGBs)

Financial integration with the global market (Japan: an open capital account allowing asset holders to benefit from higher overseas returns)

Financial stability (in Japan’s case even global financial stability, given the yen carry’s importance in global markets).

Starry skies

Let me take this one step further.

There’s much talk these days, not least among BoJ policymakers, about where Japan’s r* is (higher than 1% nominal, apparently).

But perhaps what’s at least as important is Japan’s financial stability real interest rate (or r**, as

and co-authors call the concept).Loosely speaking, r** is a kind of financial stability constraint. When r = r**, something breaks in the financial sector.

For example, r** offers a useful perspective on last year’s US banking turmoil – remember Silicon Valley Bank?

So mark-to-market assets with Japanese financial institutions could be one risk.

Or, what may matter more in Japan’s case could be a kind of financial stability interest rate differential (vis-à-vis foreign, perhaps US, interest rates). In which case, the Fed may play an important role.

Yen speculation

How will Japan navigate this trilemma? And what does this framework tell us about the yen?

Ultimately, the retreat of the BoJ from the JGB market over the long term (as it reduces purchases), means either fiscal policy is tightened; and/or private investors – domestic and foreign – increasingly absorb JGB issuance. This requires an increase in the return of JGBs relative to other (global) assets.

This should imply higher rates on JGBs, probably in (relative) real terms – adjusted for inflation. That’s the broad direction of travel.

Now, the BoJ should have considerable control over the speed of travel. They won’t want to hurry – as the bank’s officials keep emphasizing - so as not to upset the fiscal sustainability apple cart.

So here’s one way of looking at the whole thing. You want to be long yen, if you think that

the Fed is some way above neutral, and the BoJ is some way below neutral (in terms of their respective r*);

the BoJ’s r** is not much lower than its r* - which means you don’t think the unwind of the yen carry will be much of an issue anymore going forward; and you take the view that Japan’s financial sector is fundamentally sound;

and/or that further – potentially sharp – yen appreciation will not harm the economy much (perhaps because, symmetrically, in the controversy over whether yen depreciation boosts or harms the economy, you come down on the latter side);

the Fed will be sufficiently ahead of the curve to achieve a soft landing (a hard landing would mean deeper Fed cuts and most likely a global recession – a recipe for, arguably, excessive yen strength in the past).

In Castaway, the hero managed to overcome the turbulent seas at the edge of the reef and was eventually rescued by a passing ship – a large tanker.

We will know a bit more on September 18: FOMC day.

The advent of Abenomics with the re-election of Shinzo Abe in December 2012 was a major impetus for more aggressive easing. Under the leadership of governor Kuroda, the BoJ launched “Qualitative and Quantitative Easing” in April 2013 and YCC in September 2016.

These are shares in total general government debt. However, the difference between total debt and debt securities is negligible (in 23Q4 these were 1,300 trillion and 1,210 trillion yen, respectively).