Do Sell in May

The current sweet spot for stocks won't last

“Peak uncertainty” perceptions on tariffs and as yet resilient data have buoyed the stock market. That looks hard to sustain.

Photo by Patrick Weissenberger on Unsplash

“One of the hardest things in this world is to admit you are wrong.“

Benjamin Disraeli

Having rallied hard lately, stocks are now back to before “Liberation Day” levels (the S&P500 is 1% higher as of Friday, 2 May).

Two things appear to have contributed to the sharp recovery in the stock market.

a narrative of “peak uncertainty” is taking hold in markets: with current levels of tariffs being unsustainable for everyone involved – certainly for the protagonists US and China – first noises of conciliation have been heard.

US (hard) data has so far been resilient.

sees some impact from the tariffs already; still, Q1 “core GDP” expanded at a solid 2.3% annualized, while Friday’s payroll data for April comfortably beat expectations.

So far, so good?

To me, this situation looks fragile. Here are my objections.

The art of the trade deal

Trade deals will take time and even then and are likely to be partial only. I just don’t see how tariffs can return to low levels given the administration’s stated aim of generating substantial revenue from them.

notes in his latest piece[H]istory suggests that once tariffs are raised, it is hard to bring them back down. It wasn’t until 1934 that President Franklin Roosevelt passed the Reciprocal Trade Act which began the process of reversing the damage of the 1930 Smoot Hawley Act - and even then, it took the rest of the century to lower tariffs to the levels where they stood when Trump first entered the White House.

Nor can I think of a scenario that under a Trump presidency uncertainty would return to pre-Trump levels. And there will be a lot of permanent damage to supply chains.

So while I can see that for as long as the market can fantasize about trade deals the way of least resistance for stocks is up, I think reality is likely to disappoint. At best, there will be a lot of back and forth contributing to volatility.

Of course, Trump is desperate to reach an accommodation with the US’ trading partners, and will present any deal as a win. But corporates and households will look at their bottom line, and so should stock investors.

Data

And there simply hasn’t been enough time for the data to show the impact of tariffs yet.

Rather than GDP and the labor market, which are mostly backward-looking, the best we can do is to turn to forward-looking data.

How are you feeling?

Take consumer and corporate sentiment, and there let’s look at the most forward-looking parts. (Soft data tend to get looked down upon by many - I think these are circumstances where I wouldn’t dismiss them so easily.)

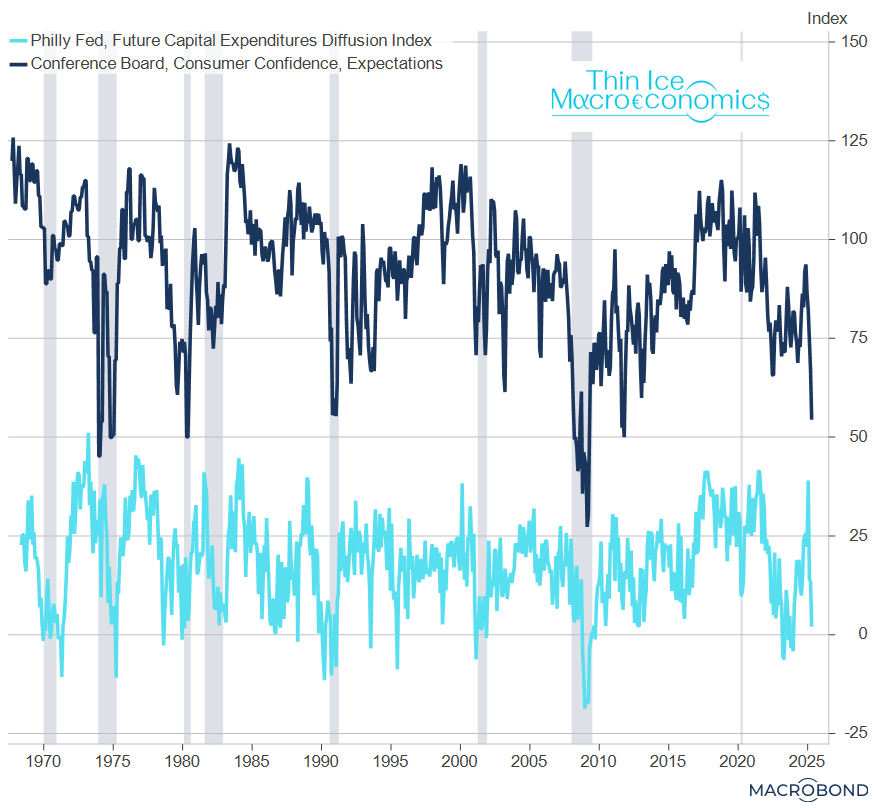

The chart below shows consumer expectations from the Conference Board; and capex expectations from the Philly Fed survey.

source: Conference Board, Philadelphia Fed, Macrobond

Both have fallen precipitously, and while they not yet at recessionary levels, they aren’t far – and that’s before the bulk of the tariffs have actually arrived in the economy.

Buffers

The stock market may also have convinced itself that the impact of tariffs won’t be so bad due to various buffers.

Yet the dollar, contrary to everyone’s expectations (including my own) didn’t appreciate – with the notable exception of the yuan of course, which is likely to weaken further. Of the remaining buffers, it’s not clear to what extent exporters’ margins can be squeezed enough to withstand 145% tariff rates.

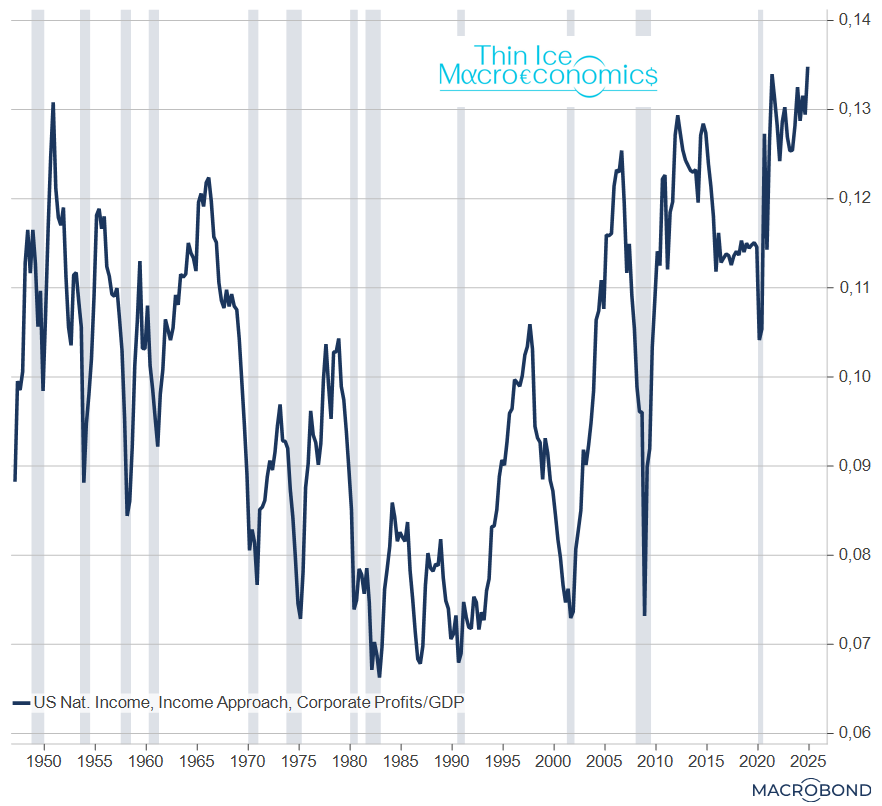

The case for US companies’ margins being ample appears to have better support – or at least is easier to demonstrate. National accounts data indicate that profits as a share of GDP are at an all time high.

source: BEA, Macrobond

The reason I’m not sure how much to make of this is that it’s not clear how much of these profits come from the tech sector (the income statistics offers no breakdown by sector).

Stock market data does suggest that about half the growth of S&P margins over the last 20 years has come from tech.

Now, it’s true that one would generally be ill-advised to assume too much of a read-across from stock market data to national accounts data.

Still, it’s plausible that tech makes up a substantial share of economy-wide profits, and that the sector’s margins are plentiful.

In any case, if profits can buffer much of the impact on Main Street, then surely that’s bad news for Wall Street?

Cheaper energy

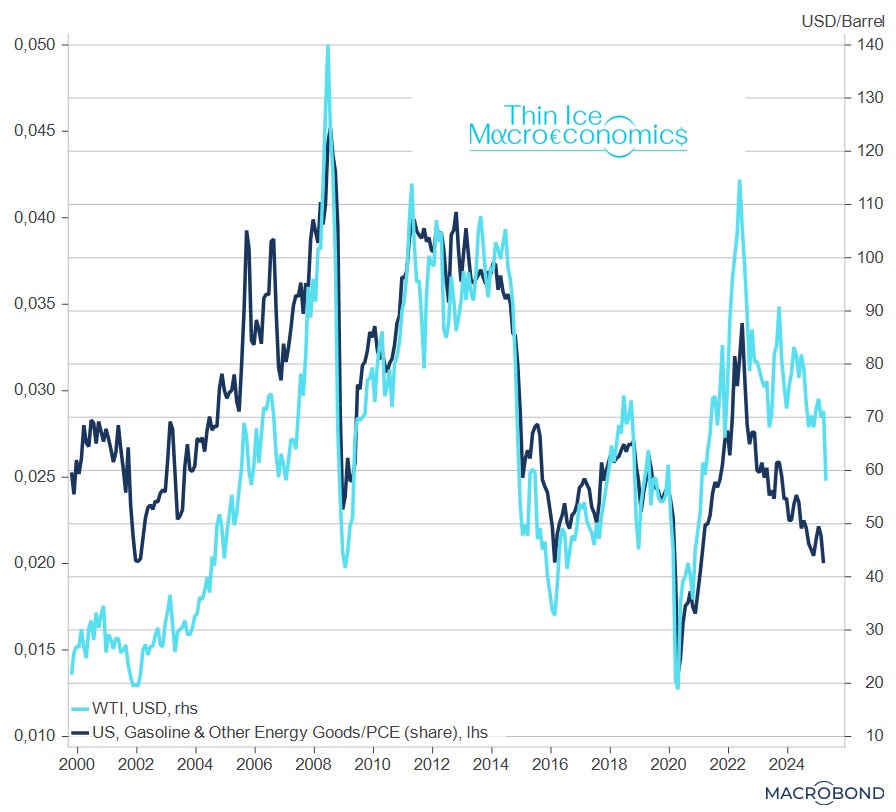

People have also pointed out that the renewed decline in the oil price will provide relief.

That’s true, but I’d question its importance at a time when energy is already down to 2% of total personal consumption expenditure. Note also the decoupling of the energy PCE share from the oil price (total expenditure surged post-pandemic thanks to buoyant income, so that a broadly constant oil price resulted in a declining energy share).

source: BEA, Macrobond

In short: I believe we are now in a sweet spot for stocks: a period where there is maximum optimism on trade deals and the reality of tariffs hasn’t showed up in the data yet.

Fed to the rescue?

It could of course be that the stock market expects the Fed to ride to the rescue.

After the April labor market report Friday, the market is pricing 3 cuts and a 30% chance of a fourth one.

Ultimately the Fed’s response should be determined by whether tariffs will be a one-off shock to the level of prices, or whether they will sustain or strengthen momentum in inflation - the rate of change in prices.

A dovish case would be: not much of a price impact (perhaps because of the buffers I mentioned above) and/or a big adverse effect of confidence on demand, which would also mean a hit to the labor market and hence probably a recession. In this case, even more than three cuts would be possible.

But I don’t see how that would be good news for the stock market.

And then there’s fiscal policy.

I argued last week that Trump needs a big fiscal win – tax cuts going beyond a simple renewal of the Tax Cuts and Jobs Act (TCJA)– to stave off recession ahead of the midterms.

And all indications are that a big package is on the cards. Budget reconciliation is aiming for 1.5 trillion, or 5% of GDP, in debt-financed tax relief on top of the TCJA.

With bond vigilantes having been awoken, a tax cut of this size could prove expensive for the US Treasury.

In any case, let’s suppose that such a package would be good news for the stock market.

It would not, however, be good news for Fed cuts.

The FOMC would have to take the fiscal impulse into account, since this is exactly the kind of thing that could turn a one-off price level increase from tariffs into a major inflationary impulse.

A full cut is priced for the July 30 FOMC meeting.

Meanwhile, US Treasury secretary Bessent wants the package done by July 4th. While the data may well have deteriorated sufficiently by then to justify a cut, the fiscal package does make a further two Fed cuts by the end of the year look like a lot.