Mar-a-Lago vs. the Fed Grand Dollar Overdraft

The next fight?

Proposals about a Mar-a-Lago accord have focused on the dollar’s role as a reserve currency, but for its exchange rate – especially in recessions – the dollar’s dominance in global funding markets becomes crucial. This suggests that any partial approach to changing the rules of the game for the dollar may be incomplete at best. More broadly, it demonstrates that the MAGA objective to structurally weaken the dollar’s exchange rate while maintaining its dominant status in the global economy is a high-wire act. The network of dollar liquidity swaps with other central banks could be the next fault line between the Fed and MAGA.

Photo by Joshua Hoehne on Unsplash

“The interplay between reserve status and the loss of manufacturing jobs is sharpest during economic downturns. Because the reserve asset is “safe,” the dollar appreciates ... when aggregate demand suffers a decline, pain in export sectors get compounded by a sharp erosion of competitiveness.” S. Miran (chairman of the Council of Economic Advisers)

[This piece is my second on the Mar-a-Lago accord. Last week I looked at whether the euro could supplant the dollar as the world’s dominant currency.]

In its quest to protect manufacturing employment, MAGAnomics has focused on the dollar’s role as a reserve currency.

Accordingly, proposals for a Mar-a-Lago accord to weaken the dollar’s exchange rate have centered on reserve holdings of US assets – for example, “terming out” these holdings into “ultra-long duration” Treasury securities.

However, being the preferred currency for those who manage official reserves is just one dimension of the dollar’s dominant role in the international financial system.

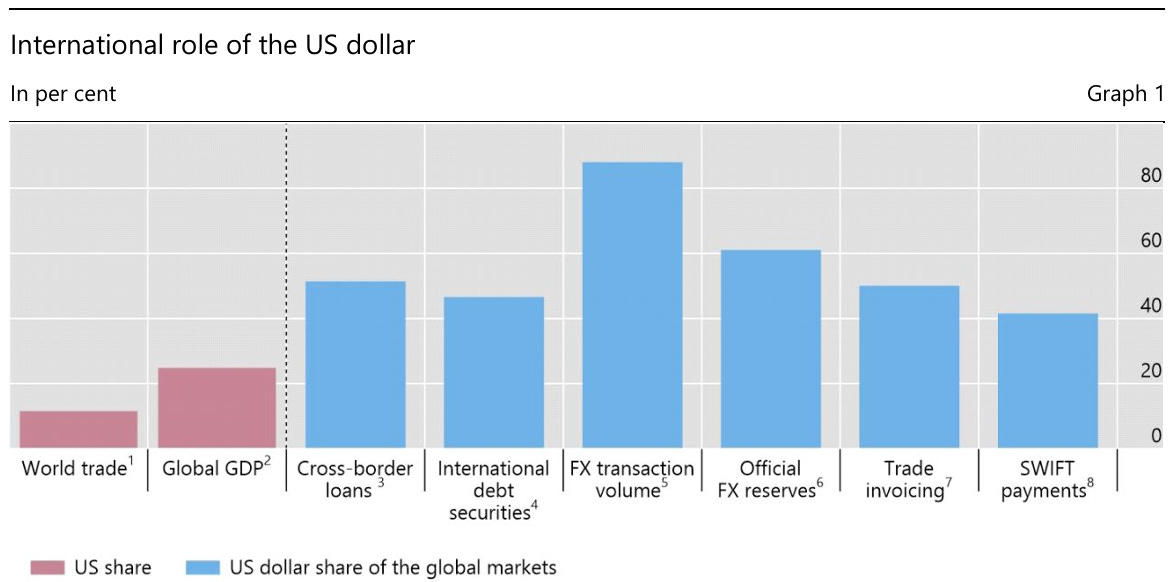

The dollar is also a vehicle currency for foreign exchange transactions, an invoicing currency for global trade, and a funding currency: entities all over the world, financial as well as non-financial, use it to borrow.

The below chart from the Bank of International Settlements (BIS) is somewhat dated but conveys the point.

Source: BIS (2019), US dollar funding: an international perspective

Rubik’s cube at Mar-a-Lago

In fact, the dollar’s different functions reinforce each other.

A non-US importer of widgets may need to pay in dollars, for which she may want to hold a US dollar deposit account. This means her bank will have more dollar-denominated liabilities, which in turn forces the central bank to accumulate dollar reserve assets.

This makes the dollar’s dominant position in the international financial system look like a Rubik’s cube.

You rotate along one dimension to bring about the desired combination of colors, and the colors will change on other sides, too – not necessarily in the desired way.

I’m saying this because MAGA are trying to have their cake and eat it: weaken the dollar on a sustained basis while maintaining its role as a global reserve currency. This is going to be tricky.

My concern is that an approach which singles out (any) one dimension of the dollar’s dominant role may prove inadequate.

Perhaps more to the point, identifying and orchestrating the right interventions may be so difficult – or the MAGA approach so heavy-handed – that the dollar weakens but loses its dominant status as well.

US dollar funding 101

Take the example of US dollar funding markets – an important part of the plumbing of the global economy.

(As is often the case with plumbing, you only know it’s there when it doesn’t work.)

Just about everybody participates in the US dollar funding markets – both US and non-US entities.

At any given point in time, a myriad of banks, other financials, corporates, official institutions etc. move dollars around the world to finance international trade, invest, leverage, borrow and lend cross-border, speculate and hedge in FX, etc.

A large amount of this takes place outside the US.

According to a BIS report, “[t]he amount of outstanding ... debt securities [issued outside the country where the borrower resides] and cross-border loans that are denominated in US dollars is $22.6 trillion as of Q4 2019 … corresponding to about 50% of all outstanding international debt securities and cross-border loans.”

By comparison, official reserves denominated in US dollars – the focus of MAGA – were 6.7 trillion in 2019Q4 (6.8 trillion in 2024Q3).

That is, international US dollar funding is three times the size of official reserve holdings.

Recessions and the exchange rate

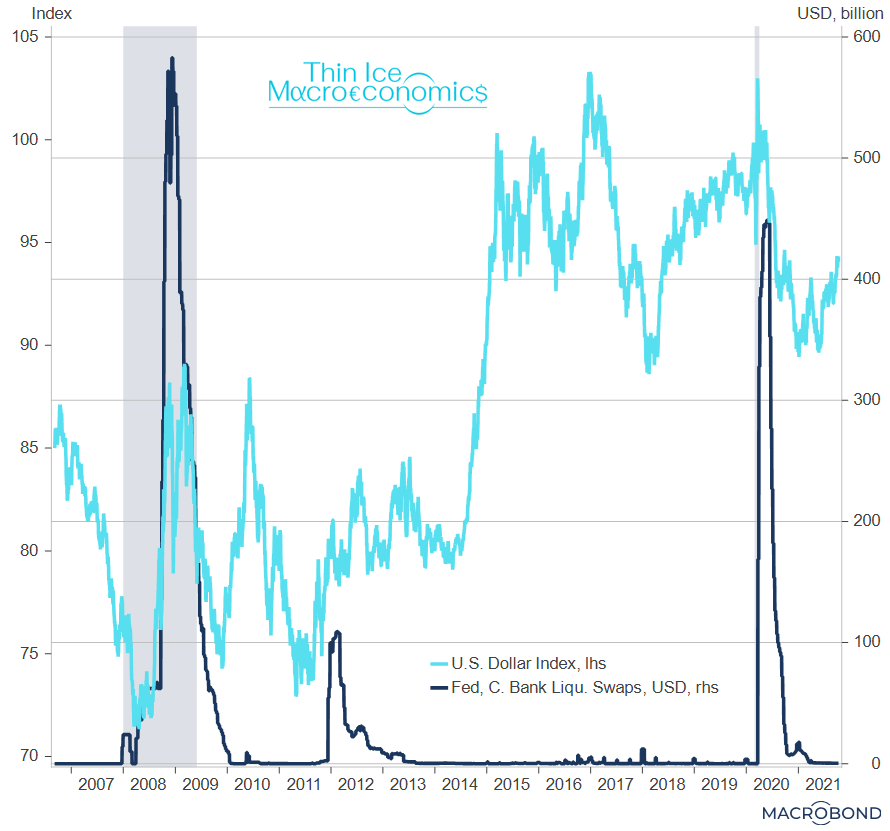

As identified in the intro quote, the dollar strengthens during recessions (shaded grey in the chart below) and/or periods of financial turmoil due to a flight-to-safety effect very much related to the dollar’s role as the predominant international currency.

Source: ICE, NBER, Macrobond

This has partly to do with the fact that there are a great many non-US players in the funding markets.

In the words of the BIS: “Most non-US entities do not have access to stable sources of funding, such as retail US dollar deposits, nor can they obtain US dollars through the US interbank market or access Federal Reserve facilities. These entities make extensive use of less stable forms of US dollar funding.”

Essentially, when things get dicey, the world scrambles for dollar assets, and the currency appreciates.

Which means: if you don’t want the dollar to strengthen too much, you need to have a – globally – elastic supply of it.

The Fed’s grand dollar overdraft

This is where the Fed, but also the global commercial banking system comes in.

Non-US banks can in principle satisfy a great deal of the global demand for dollars by offering dollar loans to their customers.

To fund those assets, however, they themselves need to have access to dollars.

During recessions or periods of financial turmoil, the normal functioning of funding markets tends to be impaired.

At such times, the role of central banks as lenders of last resort becomes important – particularly of the Fed at the center of a global network of central banks.

This works via central bank swap lines, which the Fed can use to make dollar liquidity available to other central banks. In turn, the other central banks then make this dollar liquidity available to their commercial banks.

For example, if the Bank of England has a swap line with the Fed, a UK bank can go to the Bank of England, post sterling collateral, and get US dollar liquidity.

“[T]he swap lines leverage on the “elasticity” of the Fed’s and commercial banks’ balance sheets to offset rising demand for dollar liquidity.” This “grand dollar overdraft” reflects the Fed’s critical role as a backstop for the private provision of dollar liquidity.

(The mechanics of the swaps are such that the Fed doesn’t bear any financial risk in these operations.)

In short: recession and/or financial turmoil strengthen the dollar – dollar liquidity is distributed by the Fed via its swap lines – the dollar calms down:

Source: Federal Reserve, ICE, Macrobond

For example, during the turmoil related to the outbreak of covid-19, take-up of the Fed’s swap lines peaked at 450 bn dollars.

What does the Fed achieve by doing this?

It ensures the dollar plays its role as the world’s dominant currency; and by doing so it provides the world with financial stability – a global public good.

(A public good is something that everyone benefits from, whether or not they contributed to its supply; and nobody can be excluded from benefitting from it.)

MAGA vs public goods

Now, there’s something that connects MAGA policies as disparate as shutting down USAID, exiting the World Health Organization, withdrawing from the Paris climate accords, and more generally abandoning the rules-based international order that America itself created.

It’s MAGA unwillingness to contribute to the supply of global public goods. (That this will prove self-defeating is another matter.)

So here’s the dilemma for MAGA.

Using financial repression of official reserve holders through a Mar-a-Lago accord may not resolve the problem of the dollar strengthening in recessions unless the Fed continues to provide liquidity elastically via its swap lines.

But that doesn’t seem compatible with MAGA ideology.

The next fight?

Trump’s recent executive order effectively ending the independence of federal agencies specifically exempts the Fed’s “monetary policy functions” (thank you Scott Bessent?).

The international swap lines fall under section 14 of the Federal Reserve Act which is about Open Market Operations.

It seems that we’re covered.

But then there is this sentence from the MAGAnomics manifesto: “Waiting for turnover at the Federal Reserve increases the likelihood that the Fed will voluntarily cooperate to help accommodate changes in currency policy.”

In any case, recall that the Federal Reserve Act can be changed by a simple majority in both houses of Congress.

Interesting times.

My comment on the issue, not the post. :)

https://thomaslhutcheson.substack.com/p/the-dollar-privilege-or-burden