Tariffs, Taxes, Trump and Trouble

... for the Fed and the dollar

The Trump administration cutting off the US economy’s nose to spite its face means the market can no longer have confidence that economic logic will prevail over ideology – and thus in MAGA’s overall stewardship of the US (never mind the global) economy. This casts a heavy shadow over the dollar and accentuates the Fed’s dilemma.

Photo by Gio Bartlett on Unsplash

“Double, double toil and trouble; fire burn and cauldron bubble.” W. Shakespeare (Macbeth)

Four thoughts on the “Liberation Day” tariff announcements - or rather, three and a half.

Tariff tail wags the DOGE dog: MAGA now have to go big on fiscal

My starting point: a plain vanilla extension of the Tax Cuts and Jobs Act will not result in any positive fiscal impulse – it would only prevent a negative fiscal impulse that would result from a non-extension.

Now, however, there is the need to offset

a significant loss in real income from the tariffs (= tax hike) – nerds: this is the move along a given aggregate demand curve resulting from the upward shift in aggregate supply due to the tariffs.

a hit to confidence that was already underway before the announcement, visible for example in consumer confidence data. This sentiment effect is affecting spending – nerds: this is a downward shift in the aggregate demand curve.

(While we’re on spending. We have just witnessed – after a long illness – the ignominious death of the Trump put. Or at the very least: the stock market may decide to chase the ever decreasing strike price of that put, in which case it may be time to start thinking more seriously about adverse wealth effects on consumption.)

To offset the above, the administration needs a positive fiscal impulse to stave off recession, and it needs it quickly. Offsetting DOGE cuts won’t cut it (excuse the pun), the objective will have to be a net fiscal expansion – nerds: to shift the aggregate demand curve back out.

In short, rather than tariffs being the additional source of revenue that stabilizes the fiscal situation, fiscal now has to make up for the damage wrought by tariffs: the tariff tail now wags the fiscal dog.

The combination of the tariff shock and expansive fiscal policy is what turns the initial price level shock into an inflation shock.

Which means headwinds should emerge for bonds before long. Flattening pressure on the curve should give way to steepening pressure.

Fed: on the horns of a dilemma

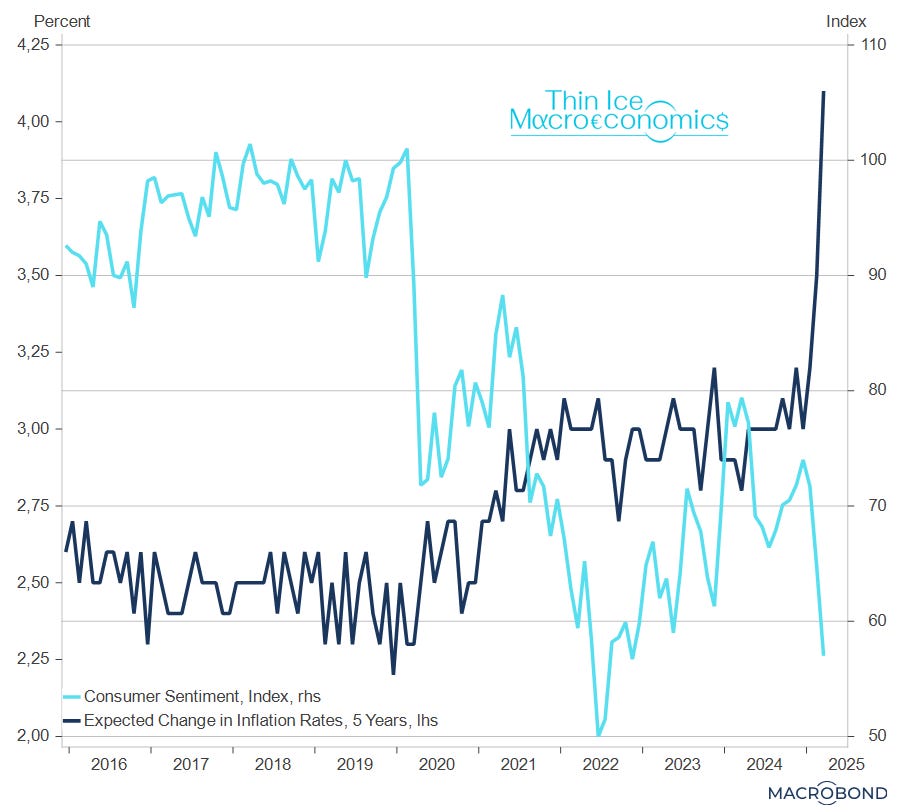

We knew the Fed’s in a tight spot even before the announcements: it’s faced with a major stagflationary shock at a time when inflation expectations are poorly anchored. If the March SEP is anything to go by, the stagflationary shock is likely to be much bigger than the FOMC expected.

Source: University of Michigan, Macrobond

I have my doubts whether the Fed can deliver as much as the rates market has priced, as quickly.

The sequencing should not be conducive to that.

Inflation should pick up quickly, probably further boosting inflation expectations. The labor market is slower to respond, and given inflationary pressures and broader confidence issues (see below) the Fed may have to wait until it sees “the white in the eyes of recession” before moving rates down.

It’s also not clear to me how much rates can go down eventually if there’s a big fiscal response coming down the line (see above).

The dollar: confidence game

There’s also much more at stake than usual.

In a break from time-honoured patterns, the dollar has weakened in a global risk-off move in response to the announcement.

This could be benign, if markets are pricing more cuts in the US than elsewhere – that’s an assessment to be made on a case by case basis, with implications for the respective dollar cross.

There’s also a less benign interpretation.

The administration has been undermining confidence in the dollar for a while now, not just by trying to talk the dollar lower or by (on-and-off) pressure on the Fed to ease policy, but by floating ideas to weaken it structurally, some of these involving outright reprofiling of US Treasury debt.

Thus, the unusual weakening of the dollar may be evidence of an erosion of market trust in the administration and its policy framework.

The administration cutting off the US economy’s nose to spite its face means the market can no longer have confidence that economic logic will prevail over ideology – and thus in the administration’s overall stewardship of the US (never mind the global) economy.

Which means that markets will be exceptionally sensitive to the Fed.

If the Fed doesn’t stand its ground now, markets may see this as the thin edge of a “fiscal dominance”/political pressure wedge creeping into US monetary policy.

The administration’s words and actions being what they are, the Fed may be the last line of defense of the dollar’s reserve currency status in the minds of investors.

More broadly: can you have a global reserve currency if you destroy the very order – and orderliness and predictability – on which the currency’s status is based?

Global recession? Perhaps. Global rebalancing? For sure

We have all seen the charts about what happens to the US’ effective tariff rate. This shock is not to be taken lightly. I share the worries about a global recession.

There’s an immediate severe hit. Negotiations will be on a country-by-country basis and are likely to be protracted (and in any case there’s a 10% tariff on everyone, for sure).

In the “rest of the world” there will be fightback – through domestic policies, monetary and fiscal.

I argued last year that tariffs are dovish ECB, and I think this argument generalizes to most economies – certainly the ones with trade surpluses vis-à-vis the US – since the impact will be net disinflationary.

In turn, that will make room for a fiscal response.

The European example is instructive. Germany has made the announcement, but for the economy this is a 2026 story.

Fiscal policy is like the cavalry: it often arrives late. For global yields, this means down first, up next. When the dust settles, yields will be higher.

As the trade surplus countries respond with fiscal policies, their national (excess) saving will shrink. Domestic demand will become more important, also making economies more resilient to external shocks.

A more balanced global economy should be the result before too long.

The logic for an expansionary US fiscal response to the tariffs may be there, but is that something the current administration would really be inclined to pursue? (Recognizing that extending the 2017 tax cuts won’t be expansionary.) Maybe any fiscal expansion policy comes from Europe or elsewhere outside the US.