The Trickiest Trump Trade

The Trickiest Trump Trade

Trump wants a weak dollar - are markets right to doubt him?

Trump’s stated policies and objectives - weak dollar, tax cuts, tariffs, and a lower trade deficit - are mutually inconsistent and are likely to result in a stronger dollar: markets are right to question his weak USD rhetoric.

Unorthodox policies may be feasible but would make financing the fiscal deficit more expensive and/or imperil the dollar’s reserve currency status: the US’ privilege may be exorbitant, but not unlimited.

Much has been written about the economics of a potential Trump 2.0 administration. Meanwhile, the market grapples with any number of Trump trades, from curve steepeners to sector plays in equities - even if the importance of the Trump element in some of these trades isn’t always obvious.

These trades have waxed and waned in response to the dramatic developments of the last few weeks.

One key question with implications well beyond financial markets is of course the dollar.

Trump and his team favor a weak dollar. But they also have other objectives.

Tariffs, together with the weak dollar, are meant to protect US manufacturing employment, and lower the trade deficit.

Tax cuts are also high on the agenda.

But are tariffs compatible with a weak dollar? And what do tax cuts mean for the trade deficit? And for the currency?

In short: what about the mutual consistency of the Trump policy objectives?

Tariffs and the dollar

We have recent experience. To jog my memory, I did a bit of plotting.

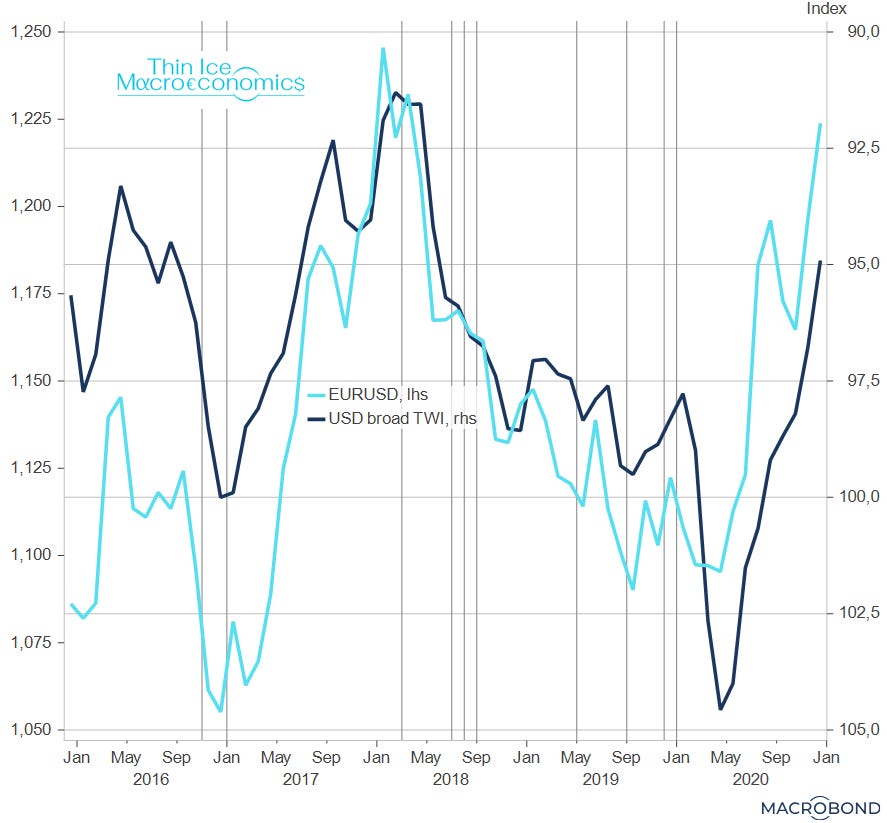

The chart below shows two measures of the dollar: a broad trade weighted one (“USD broad TWI”, indexed at 100 in December 2016); and the dollar against the euro (“EURUSD”). (Note that I’m using the market convention of dollars per euro: when this goes up, the dollar weakens.)1

I’ve also added vertical lines for various Trump- and tariff-related events: November 2016 for the election, January 2017 for his administration taking office; the rest are related to tariffs.

source: Macrobond, Federal Reserve

The first thing that’s striking is that the dollar is strong as Trump takes office in January 2017 (in fact, at a multi-year high).

It then turns around and depreciates (remember when the lines go up, it’s a depreciation of the dollar). From 1.06 in December 2016, EURUSD reaches 1.25 on the eve of the China tariffs in January 2018.

While there were plenty of reasons for this depreciation, e.g. relative monetary policies and more robust global growth, the administration’s rhetoric on its desire to see a weaker dollar also seems to have contributed to a softer currency.

In 2018, the tariffs arrive.

This coincides with a multi-month appreciation trend that didn’t really reverse until some months into the covid pandemic. Again, in macro there’s hardly ever a single cause for anything, but the tariffs contributed to a strengthening of the dollar. Indeed, this is consistent with the econ textbooks.

Tax cuts and the trade deficit

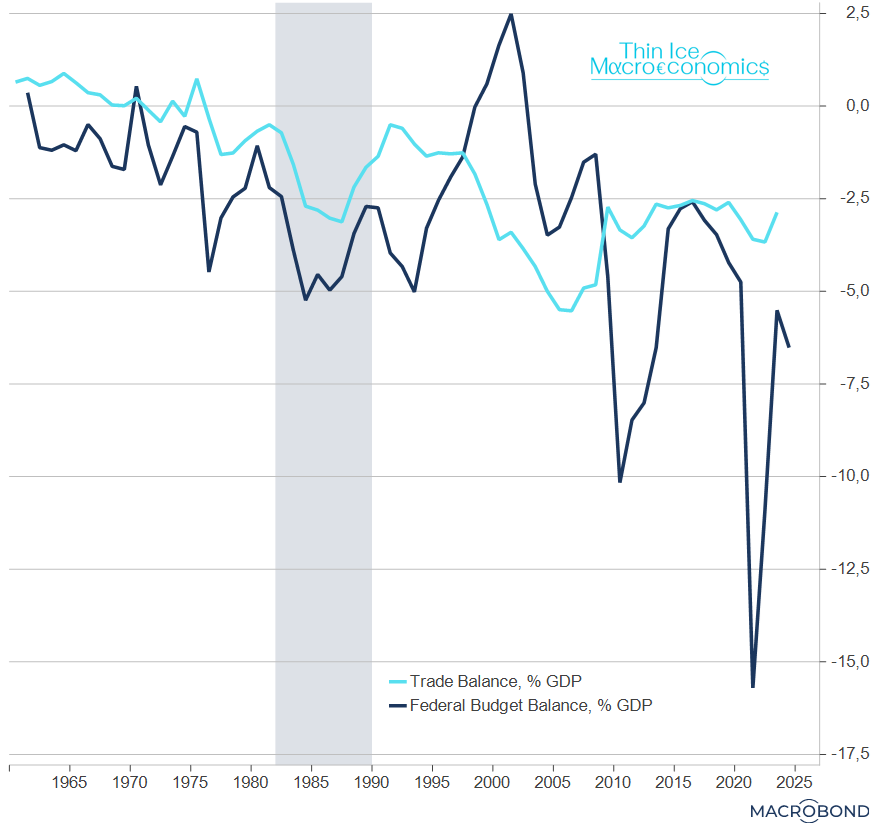

I’m old enough for the 1980s Reagan twin deficits (budget and trade) to have featured prominently in my macro education – see the shaded area in the chart below (those were the days – isn’t it just amazing what level of deficits people thought were a big deal back then?).

source: Macrobond, US Treasury, BEA

So the Reagan tax cuts blew a hole in the trade balance.

Since then, the correlation has weakened somewhat but is still positive overall, about 0.35 for the whole sample: (larger) budget deficits tend to be associated with (larger) trade deficits.

(As an aside, the chart tells us that what the budget deficit does to the trade deficit also depends on the reasons for the fiscal expansion: if the budget deficit is the result of a massive domestic recession, like the GFC of 2008-9 or covid in 2020-1, the trade deficit doesn’t widen much. If it is due to a discretionary fiscal impulse, like the Reagan tax cuts, the trade deficit is more responsive.)

Tax cuts and the dollar

The Reagan twin deficits are also a good case study on the currency effect of fiscal deficits. The strong “Reagan dollar” resulted in the 1985 Plaza Accord between the US, France, Germany, the UK, and Japan, to weaken it.

But we need not go that far back in time at all.

The dollar is currently strong because of the US policy mix: expansionary fiscal policy and tight monetary policy. Tax cuts would, more or less, be more of the same, forcing the Fed to keep rates high (or higher than they would otherwise be) to restrain inflation.

A strong dollar would be the result. Again, this is all macro 101.

Conclusion: there are mutual inconsistencies between the Trump team’s objectives. You can’t have tax cuts, a weaker dollar and a smaller trade deficit, or tariffs and a weaker dollar. The broad thrust of these policies is for a stronger dollar - markets are right to discount the weak dollar rhetoric.

Unorthodox options

According to the press, a series of other policy options are being considered in the Trump camp to weaken the dollar.

I will call these policies “unorthodox” because they are either unusual (in the sense of being used infrequently), or because they would challenge the established policy framework outright.

One possibility could be FX intervention – sell dollars.

Unlike the case where a country attempts to strengthen its currency, domestic authorities can in theory keep intervening to weaken it forever.

In the former case, the country needs to have enough foreign currency reserves to sell. In the latter case there are no limits to how much of one’s own currency one can create.

So FX intervention is in principle perfectly feasible. But weakening the dollar through FX intervention would be a problem for the financing of the budget deficit.

Why would a foreign investor buy US government debt if she knows that the value of that claim, in her own currency, would fall? Interest rates on the debt would have to increase – by the amount of expected depreciation (probably plus a risk premium).

This would also be true in the case of a hypothetical “new Plaza Accord” to weaken the dollar (whatever one may think of the likelihood of such an accord).

A tax on foreign purchases of US assets would be similarly counterproductive for the financing of the deficit.

The general point: it’s always possible to restrict capital flows – especially inflows – but the reduced availability of foreign capital will make financing the budget deficit more expensive.

In any case, if the objective is to have a weaker dollar, why penalize countries for moving away from the greenback? After all, that could weaken the dollar durably.

It’s not clear to me that one can have one’s reserve currency cake and eat it.

Another option may be to lean on the Fed to keep rates low(er). This would probably have to come together with QE, to prevent bond rates from rising.

That would result in high(er) inflation.

Again, perhaps more important would be the question of how to finance the fiscal deficit when (inflation-adjusted) interest rates are (too) low – in particular, would foreign investors still flock to buy US Treasury paper?

And wouldn’t restricting the Fed’s independence endanger the dollar’s reserve currency status?

The privilege the US enjoys from having the world’s reserve currency may be exorbitant, but it is not unlimited.

Photo by Adam Nir on Unsplash

To match this, I had to invert the axis on the broad dollar index as the index is constructed such that an increase is a stronger dollar.