Trump Could Make Europe Great Again

Time for peak pessimism on Europe

This is my last post ahead of the holidays, and it’s going to be a bit different.

Think of it as year-end op-ed piece.

My case: we should be close to peak pessimism on Europe. From an investment perspective, there may yet be better entry levels before actually “buying Europe”. But it’s time to turn cautiously positive on the continent in a long run view.

Photo by Christian Lue on Unsplash

“Everything has to change, for everything to stay the same.” Giuseppe Tomasi di Lampedusa, Il Gattopardo

Europe’s “holiday from history” ended with Russia’s full-scale invasion of Ukraine, but many Europeans and their governments had been trying to postpone dealing with the implications.

The re-election of Donald Trump at the head of a political movement that makes no secret of its ideological affinity with Vladimir Putin has finally shaken Europe out of its torpor. (One unavoidable realization being that Europeans have no god given right to live forever under the American security umbrella.)

The European disease

No need to belabor this.

Europe is facing multiple crises, all of which converge on growth: it’s clear that Europe has a growth problem.

Where does it come from? The consensus view is that it’s a supply problem – overregulation, bureaucracy etc. stifling Europe’s growth potential – and I don’t disagree.

In fact, I don’t have much to say here about the required supply-side reforms in Europe. These things have been talked about extensively for a long time, and the Draghi report discusses them thoroughly.

What’s often overlooked, though, is that Europe also has a chronic demand deficiency problem.

Why does that matter?

Supply and demand go hand in hand

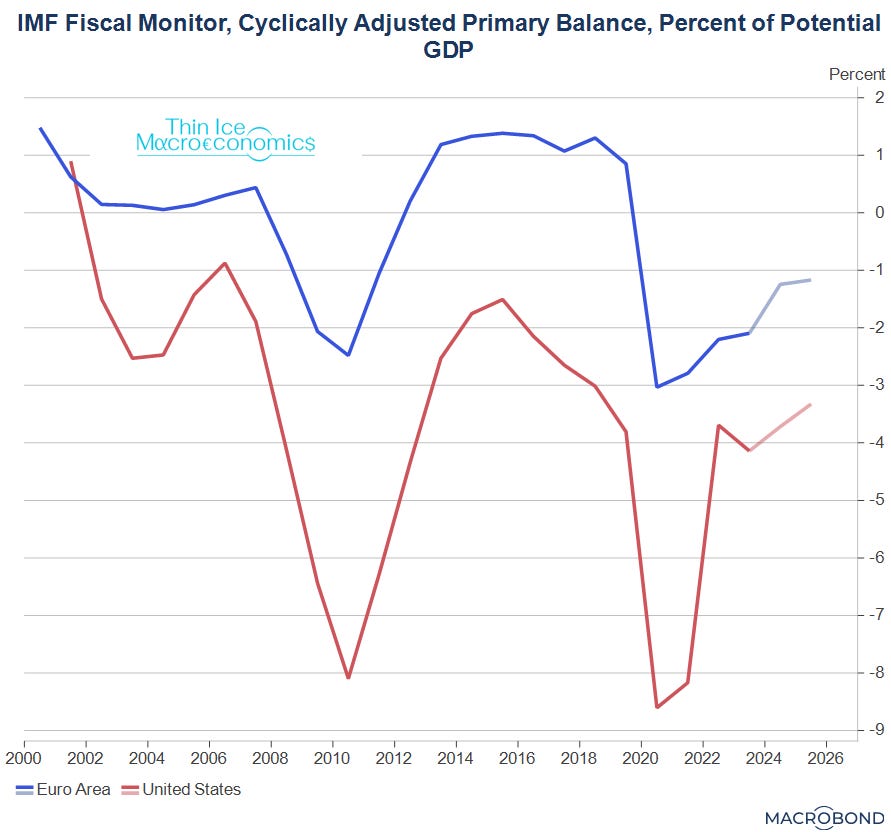

First, demand creates supply. Not only in my perception is the US’ superior productivity performance partly attributable to the fact that monetary and fiscal policy are consistently running the economy hot.

For example, the primary fiscal deficit adjusted for the economic cycle is consistently several percentage points greater in the US than in the euro area – the Americans have an exorbitant privilege, and they’re using it.

source: IMF

The other side of this coin is that Europe’s chronically poor productivity is also partly attributable to deficient demand. (I hasten to add that demand is not the key explanation of the two economies’ productivity performance!)

Second, demand impinges on the political will to create supply – i.e. to reform.

When the economy is growing (boosted by sufficient demand), it’s easier to enact structural reforms.

An ideal political “compact” would boost demand (my preference: mostly through lower taxes, alongside the necessary increase in defense and investment spending, incl. on decarbonization); this would raise incomes and lower unemployment risk, making supply-side reforms easier.

Making a virtue of necessity

Going forward, boosting demand will be the main way for Europe’s saving and current account surplus economies – and hence for much of the euro area – to grow.

No news here – the days of mainly export-led growth are probably over: China has leapfrogged the continent’s car industry and has emerged as a serious competitor in important sectors like chemicals and machinery. Their main export market, the US, is about to slam tariffs on European goods.

Perhaps more importantly in the long run, demographics will force a decline in national saving and in excess foreign asset accumulation – and hence export surpluses (Germany’s net foreign assets are 70% of its GDP, the Netherlands’ 54%). Incidentally, this also promises much-needed (further) internal rebalancing of the euro area economy.

What’s more, there is the need for Europe to establish a deterrent against further Russian aggression.

Defense spending is set to rise even more. While there are still some countries that don’t fulfil the NATO 2% of GDP defense spending target, the talk in Brussels (conveniently also the location of NATO headquarters) these days is for a 3% target eventually.

Architecture lesson

Part of the reason for the excessive fiscal restraint in Europe in the past has been the common currency’s inadequate architecture, which resulted in the euro area crisis of 2008-13.

As some countries ran out of fiscal space, there was no fiscal backstop to prevent an excessive demand contraction in the economies under market pressure (I’m cutting a long story short here).

Worse, the “strong” countries failed to use their fiscal space to provide an offsetting fiscal expansion to the contraction of the crisis countries in order to balance demand in the euro area. The result was a “downward adjustment”: many years of lost growth – and damage to supply, particularly in the crisis economies.

(None of which is to deny the structural, homegrown reasons for the poor productivity performance of Southern European economies.)

Demand boost coming

There have been, by now, significant improvements in the architecture of the euro area (although more remains to be done).

Perhaps more importantly, German fiscal expansion is underway. The particulars of this will depend on the outcome of the federal election in February, and there are enough potential complications on the way as to warrant a separate piece (this is not a promise!).

But the direction of travel is towards more of a fiscal effort from Germany, probably via a reform of the debt brake (you read it first from me of course!). While that won’t be felt in the economy before 2026, it should nonetheless constitute a significant change in the way fiscal policy is run in Germany.

The greater German fiscal effort is of course a key part of the increased domestic demand and internal rebalancing story I just mentioned.

Not entirely coincidentally, it should also satisfy incoming US Treasury secretary Scott Bessent, who is very right on the issue of Germany needing to expand domestic demand (but it may not please his boss: it’s hard to see Europeans buying more American cars).

More broadly, Europe will continue to face the problem that fiscal space is unevenly distributed.

In principle, this would call for a federal solution, especially when it comes to funding Europe-wide public goods like defense: issuance of debt under “joint and several” liability.

Cometh the hour, cometh the money

Now, this Hamilton-admiring European federalist acknowledges that such debt issuance is politically unattainable anytime soon.

But there has been an important quasi-federalist precedent: the NGEU (aka “recovery fund”), set up as a response to the pandemic. Plans to set up a 500bn euro defense fund (potentially with the participation of non-EU countries) suggest that the modus operandi of setting up “pots of money” for specific purposes continues to be the way forward.

(Incidentally, the 500bn is about 3.5% of euro area GDP or 3% of EU-27 GDP – by no means peanuts, although I’d expect a meaningful chunk to be spent on US-produced military hardware as part of an eventual trade deal.)

Peak regulation in sight

Back to supply.

The road to every improvement starts with recognition of the problem.

My claim: the problem – of overregulation, excessive bureaucracy etc. – is sinking in with most of the reasonable segment of Europe’s political class, and with many voters. (Yes, in some countries faster than in others.)

The lack of growth is impossible to overlook, and the Draghi report touched a nerve.

Still, political leaders might have gotten away with ignoring it (after praising it), if wasn’t for Trump 2.0. The incoming US administration’s aggressive deregulation drive has added pressure on European politics to follow suit.

Peak regulation is in sight.

(This being Europe, nothing is straightforward of course. For example, the EU Commission’s omnibus bill to reduce bureaucracy has gotten held up. Still, the point is that such a bill is being prepared.)

Back against the wall

There’s nothing like a crisis to focus the mind. With its back against the wall, I expect Europe to start moving in the right direction soon.

The road will be rocky, with twists and turns, difficulties and setbacks. In the short term, some things may well get worse before they get better.

Policies will probably never be fully adequate, but it’s important not to use the wrong benchmark.

Legitimacy in Europe still rests with the individual countries. There are overlapping political geometries, with both confederal and federal elements (the EU, and the common currency, respectively), but Europe will probably never achieve the US’ unity of purpose.

So, I’m not predicting a rosy future for Europe. But I am predicting a future. Self-preservation is a powerful instinct I wouldn’t bet against.

Thin Ice Macroeconomics wishes its readers Merry Christmas / Happy Hanukkah / Happy Holidays and a Happy New Year!

Not sure I understand why, in the long run, Europe would want to buy American weapons to defend itself against Russians. The election of DJT was the final wake up call for the EU to become self-sufficient militarily and economically.

Indeed, we could If we -collectively- are willing to get our act together