Dispatch€s from Frankfurt: ECB Preview: Autumn Is Coming

With a cut on September 12 all but certain, the debate about an October rate cut is about to gather pace

Photo by Lukasz Szmigiel on Unsplash

While these days in Frankfurt have been sweltering hot, the mood in the economy and at the ECB ahead of the September 12 meeting is much more autumnal already, perhaps in a kind of post-Olympics blues.

Italy and Spain are doing fine, but the same cannot be said for the bloc’s two largest economies.

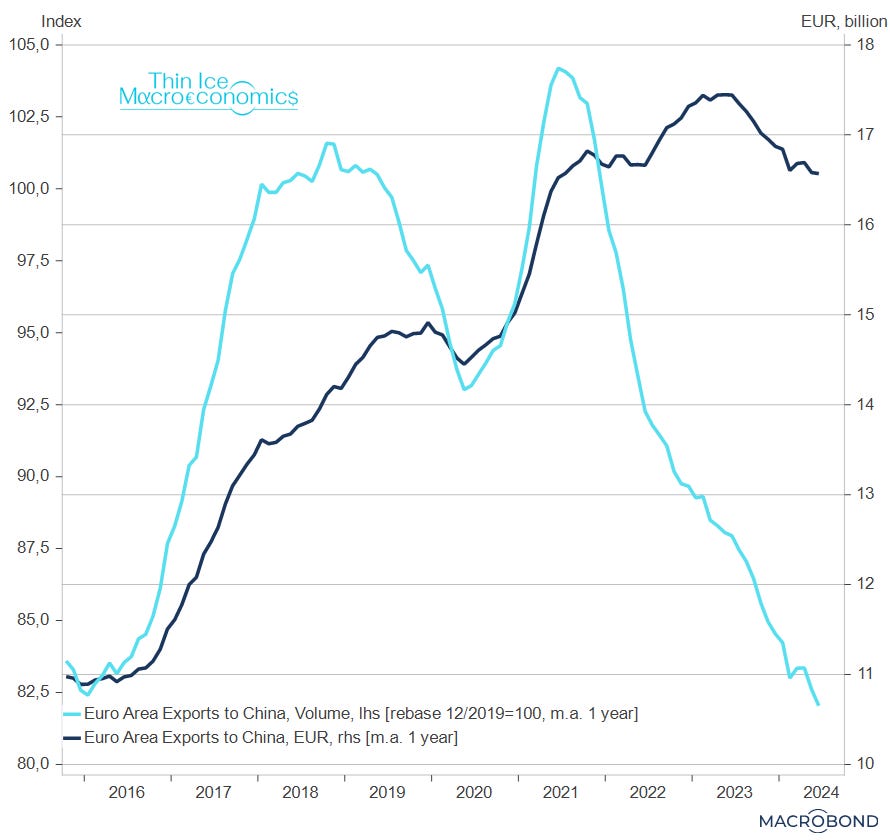

The manufacturing malaise appears to be deepening across the common currency area.

This is especially the case in Germany, where the structural challenges to the economy have thoroughly infected sentiment, evidently yet again aborting a recovery. Recent news of upcoming job cuts at corporate icon Volkswagen have shocked the country, likely knocking confidence further.

Meanwhile, the Paris Olympics bounce in the August headline PMI is likely masking underlying weakness, not only for France but also the euro area as a whole.

After September comes October

With prominent “hawks” such as Isabel Schnabel and Joachim Nagel recently having essentially signed off on a September cut – more on this below – the case for next week can now be “officially” considered closed, in my opinion.

At the same time, Schnabel and Nagel’s sign-off for September has also marked the kick-off for the discussion over the October decision.

In any case, with a September cut fully discounted by markets for a while now, what the ECB’s communication in next week’s meeting will convey about October may well be the most important takeaway of the day.

But let’s take it one thing at a time.

ECB base case on track

The key to the September 12 meeting outcome is that the data has been very much consistent with the ECB’s central scenario.

The corollary is that new vintage of ECB staff projections should not deliver anything earth-shattering: minor revisions to the near term (up for inflation, down for growth) should not affect the broad thrust of the ECB’s narrative.

In Isabel Schnabel’s words, “incoming data have broadly confirmed the baseline outlook, bolstering our confidence that conditions remain in place for inflation to fall back to our 2% target by the end of 2025”.

I take that to mean that she – and Joachim Nagel (“the worst is over”, inflation is “on the right track”) – agree to proceed with a cut next week.

This leaves the spotlight on communication.

Don’t encourage them

My expectation is that communication will be calibrated so as not to propel market expectations further towards a cut in October.

Let me explain.

I think here the attitude of the hawks is key.

I believe both Schnabel’s and Nagel’s comments were made with a view to the October meeting. More specifically, they were trying to arrest momentum towards an October cut, both in market pricing and in the governing council discussion.

(Schnabel: “Given that the path back to price stability hinges on a set of critical assumptions, policy should proceed gradually and cautiously.” Nagel: “a timely return to price stability cannot be taken for granted. Therefore, we need to be careful and must not lower policy rates too quickly.”)

Both point out that in their view there are risks of resurgent inflation and, consequently, the ECB shouldn’t rush.

I see this as a sign that the discussion about an October cut is gaining momentum inside the council.

Precommitment prevention

Their early pushback has two objectives, in my view.

One is of course the October decision itself. By articulating early pushback and pleading for gradualism – this should be the quarterly, projections-accompanied rhythm that the council seems to have implicitly agreed upon so far – they are raising the bar (= burden of proof) for an October move.

The other is next week’s communication. Having laid down a marker for the October decision (“we oppose a cut, at least as of now”), the implication has to be that they would oppose communication suggesting a cut in October.

This is with good reason.

They likely want to avoid a repeat of the run-up to the June meeting, when the governing council had essentially pre-committed to a cut, painting the ECB into a corner and ultimately forcing it to deliver despite a wobble in the data.

The other side of the same coin is that they want to avoid September communication that will encourage market expectations for October, in order to avoid pressure to deliver on those expectations for fear of disappointing the market. That’s why in her speech, Isabel Schnabel also took issue with the market pricing.

Fight the Fed

Last but by no means least, we have the Fed (a former boss of mine used to write “it ain’t over till the Fed lady sings”).

It seems likely that momentum in the market towards pricing a 50bp Fed cut will provide a tailwind for the market pricing an October ECB cut (I’m writing this before the August US labor market report).

ECB governing council members will no doubt be cognizant that chair Powell at Jackson Hole set a low bar for rapid rate reductions (“do not welcome” further labor market cooling + “ample room” to respond).

Schnabel and Nagel are thus trying to pre-empt a situation where a 50bp move by the Fed one week after the ECB automatically creates pressure in the governing council - as well as expectations in the market - that the ECB will have to follow up with a cut in October.

It is in this context that I would interpret Isabel Schnabel’s comment about the ECB having gotten a head start with the June move: “In the euro area, as we gained confidence in the projected disinflation path, we decided to start dialling back the degree of policy restraint earlier than central banks in other advanced economies. But the earlier monetary policy shifts in response to forward-looking signals, the more cautious and gradual it can afford to be on the way back to (an unknown) neutral.”

My translation: “Everyone [= markets and governing council colleagues], please let’s not forget that we have also done our 50bp [June+Sep], so we would be under no obligation to chase the Fed.”

(On the substance of the argument, I’m not sure I agree: the June cut has been amply – if ex post – justified by the data. If it has not, there should be no September cut. So having started earlier is now moot, and the discussion about the appropriate stance of policy can start from a zero base.)

Communications compromise

What does that mean in terms of specific language on September 12?

If my interpretation of hawks’ intentions is right, a viable compromise on communication could be a “unanimous cut” in exchange for wording that is not prejudicial for the (pricing of the) October outcome.

Thus, we should hear:

Risks to growth tilted to the downside, alongside a recognition of the loss of momentum in the euro area economy

A general, if vague, easing bias remaining in place (e.g. “the direction is clear”)

data dependence (e.g. “we’ll decide meeting-by-meeting on the basis of the data”)

Fed-independence of ECB decisions (e.g. “we are data dependent, we are not Fed dependent”)

ultimately non-committal about October (e.g. “we’ll cross that bridge when we get there”).

“Wide open” dovish

If, instead, President Lagarde uses the “wide open” language to refer to the outcome of the October meeting (as she did in July for the September outcome), it should be taken as dovish by the market.

That’s because there is an important asymmetry when it comes to this wording.

With the council having implicitly guided markets for a quarterly pace of cuts for some time now, markets – correctly – ignored Christine Lagarde’s “wide open” in July, expecting a cut in September. That is, for a meeting in which a cut was expected “by default”, “wide open” was not taken as hawkish.

However, for a meeting not expected to result in a cut by default, communicating that the outcome is “wide open” should be seen as a dovish sign, likely adding impetus to market expectations of a cut.

October cut?

Actually, what chance an October cut?

Back in early August I laid out a framework for an October cut, which I’m still comfortable with. In brief, this is a question about whether the recovery will stall outright, or worse – I don’t think merely subdued growth rates will do – and/or whether there will be news or data to question the inflation trend on the downside.

Most likely, this means another shock is probably needed.

We are not lacking candidates.

source: Eurostat, Macrobond, Thin Ice Macroeconomics

It could be the global economy losing steam, or China, or domestic sentiment – households have been increasing saving, rather than consuming1 - or a number of other factors.

source: Eurostat, Macrobond, Thin Ice Macroeconomics

As of today, I would still put the odds of a cut in October at no more than one in three.

I think Nagel and Schnabel will be right in the end.

Data on the euro area household saving rate for 24Q2 were not yet available at the time of writing. However, France and Germany have already published 24Q2 household saving rates, and they have increased.

Great overview about the possibility of October cut! However, I believe economic conditions in the Eurozone are less favorable compared to those in the United States. Today's industrial production data from Germany further highlights the overall fragility of the Eurozone. In my opinion, there's still enough time for Schnabel and Nagel to reassess their stance before October.